Over one million Americans face bankruptcy filings each year, with Michigan ranking among the higher rates in the nation. When debt becomes overwhelming, understanding all available options becomes crucial for protecting credit, assets, and future financial stability. Whether considering legal bankruptcy, debt settlement, or credit counseling, knowing the rules and consequences can help Michigan residents make the best decision for their circumstances.

Defining Bankruptcy and Debt Relief Options

Bankruptcy represents a critical financial lifeline for Michigan residents overwhelmed by unmanageable debt. Bankruptcy is a legal process designed to help individuals and businesses eliminate or restructure their financial obligations when they can no longer meet monthly payments. According to the Michigan government guidelines, bankruptcy should only be considered after exhausting other financial strategies like budgeting and credit counseling.

When traditional debt management fails, individuals have multiple debt relief pathways:

- Bankruptcy Filing: Provides legal protection and potential debt discharge

- Debt Settlement: Negotiates reduced payoff amounts with creditors

- Credit Counseling: Develops structured repayment strategies

As an alternative to bankruptcy, debt settlement negotiates with unsecured creditors to reduce total debt obligations. This approach can potentially reduce debt by approximately 50% and allow settlement through lump sum or structured payment plans. However, it lacks the automatic legal protections that bankruptcy provides.

Michigan bankruptcy filers must complete mandatory steps:

- Attend a government-approved credit counseling class

- Complete a debtor education course before debt discharge

- Undergo comprehensive financial documentation review

Important Considerations: Bankruptcy carries significant consequences, including potential credit score damage, possible loss of personal assets, and future challenges obtaining housing, insurance, or employment. It remains a last-resort strategy for those facing genuine financial hardship with no alternative resolution.

Chapter 7 Bankruptcy: Liquidation Process Explained

Chapter 7 bankruptcy, often called liquidation bankruptcy, provides individuals with a powerful legal mechanism to discharge unsecured debts and obtain a fresh financial start. Unlike other bankruptcy options, Chapter 7 involves selling non-exempt assets to repay creditors, allowing qualifying Michigan residents to eliminate most outstanding financial obligations quickly and efficiently.

Key characteristics of Chapter 7 bankruptcy include:

- Total debt discharge for eligible unsecured debts

- Rapid process typically completed within 4-6 months

- Immediate automatic stay preventing creditor collection actions

- Potential elimination of credit card, medical, and personal loan debts

Understanding potential liquidation mistakes is crucial for Michigan residents considering this bankruptcy option. The process requires passing a means test that evaluates your income against the state’s median household income. Individuals earning below the state median are generally eligible, while those earning above might need to explore alternative bankruptcy chapters.

The Chapter 7 bankruptcy process involves several critical steps:

- Complete mandatory credit counseling

- File comprehensive bankruptcy petition

- Attend mandatory 341 creditor meeting

- Undergo asset evaluation and potential liquidation

- Receive official debt discharge

While Chapter 7 offers significant debt relief, it carries substantial long-term consequences.

The bankruptcy remains on your credit report for 10 years, potentially impacting future lending opportunities, employment prospects, and financial reconstruction. Careful consultation with a bankruptcy professional can help determine whether this strategy aligns with your specific financial circumstances.

Chapter 13 Bankruptcy: Repayment Plans in Michigan

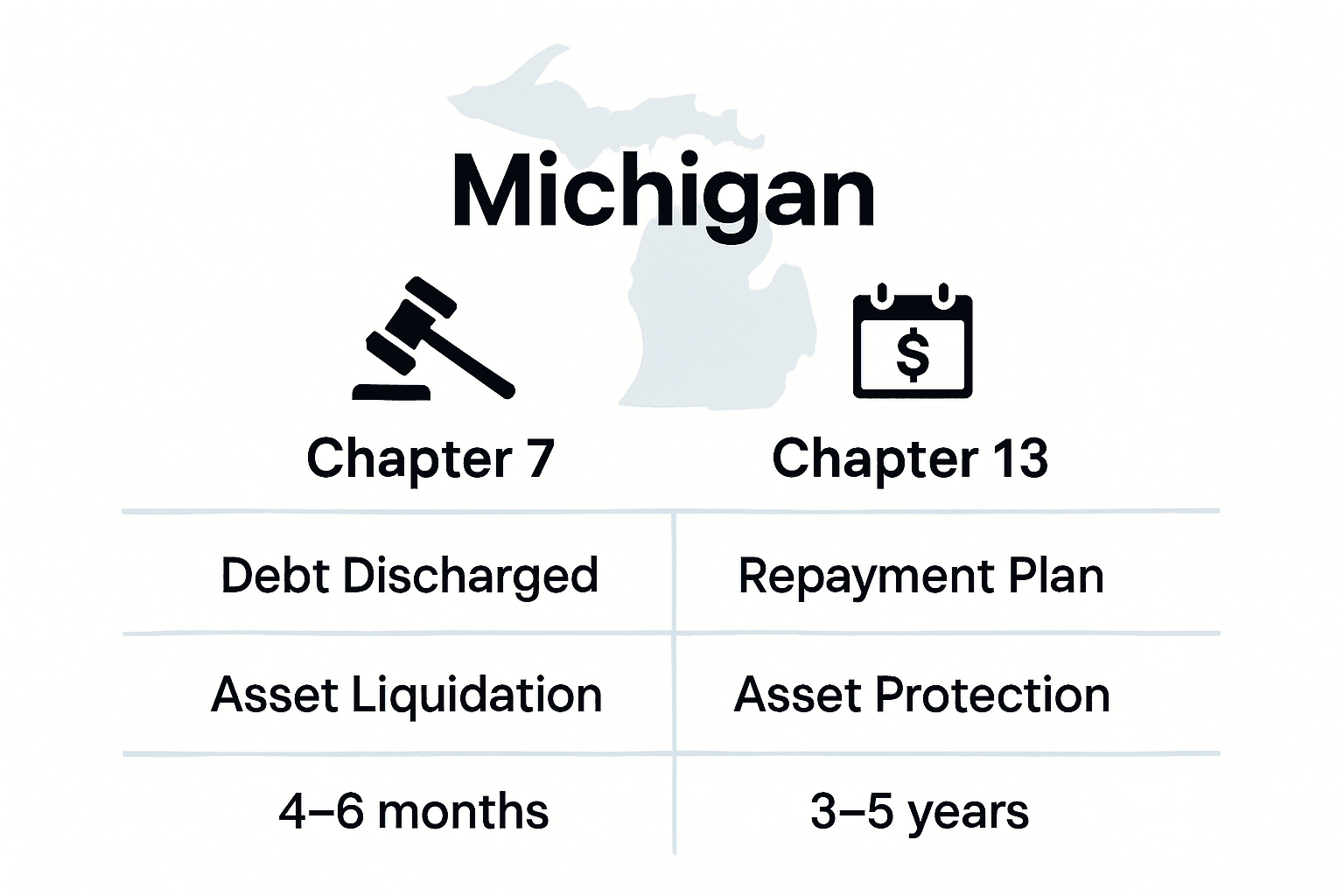

Here’s a comparison of Chapter 7 and Chapter 13 bankruptcy features for Michigan residents:

| Feature | Chapter 7 (Liquidation) | Chapter 13 (Repayment Plan) |

|---|---|---|

| Debt Treatment | Most unsecured debt discharged | Debt restructured & repaid |

| Asset Protection | Non-exempt assets liquidated | Assets protected with payment plan |

| Duration | 4-6 months | 3-5 years |

| Eligibility | Pass means test | Steady income required |

| Credit Report Impact | 10 years | 7 years |

| Protect Home/Vehicle | Limited | Strong foreclosure/repossession stop |

| Payment Plan Required | No | Yes |

Chapter 13 bankruptcy offers Michigan residents a strategic financial restructuring option that allows individuals to reorganize their debt while protecting their assets from liquidation. Unlike Chapter 7, this bankruptcy type creates a court-approved repayment plan that enables debtors to catch up on missed payments over a structured 3-5 year period, providing a lifeline for those with steady income but overwhelming debt.

Key advantages of Chapter 13 bankruptcy include:

- Prevent home foreclosure

- Stop vehicle repossession

- Consolidate multiple debt streams

- Protect co-signers from collection actions

- Potentially reduce total debt obligations

Consulting a Michigan Chapter 13 lawyer can help you navigate the complex qualification requirements. Typically, individuals must have a regular income and debts below specific federal thresholds. The repayment plan is meticulously crafted to balance creditor interests with the debtor’s financial capabilities, allowing for a manageable path to financial recovery.

The Chapter 13 bankruptcy process involves critical steps:

- Complete mandatory credit counseling

- Develop a comprehensive repayment proposal

- Submit detailed financial documentation

- Attend creditor confirmation hearing

- Make consistent payments through court-appointed trustee

While Chapter 13 provides significant debt relief, it requires strict financial discipline. Debtors must adhere to the court-approved payment plan, maintain consistent income, and avoid acquiring new debt during the repayment period. The bankruptcy remains on credit reports for seven years, presenting both challenges and opportunities for financial rebuilding.

Eligibility, Qualification, and Filing Requirements

Bankruptcy eligibility in Michigan involves complex legal criteria that vary significantly between Chapter 7 and Chapter 13 filings. Qualifying for Chapter 7 requires passing a means test that compares household income to state median income thresholds, which fluctuate based on household size. For a single-person household, this threshold is approximately $61,000, with potential flexibility for those slightly exceeding this limit through detailed disposable income calculations.

Key bankruptcy eligibility requirements include:

- Residency in Michigan for at least 180 days

- Completion of mandatory credit counseling

- Income below state median or passing means test

- No recent bankruptcy filing within specified timeframes

- Comprehensive financial documentation

As outlined by Nolo’s legal research, Michigan bankruptcy exemptions provide critical protections for filers. Frequently asked questions about the filing process can help clarify complex requirements. Exemptions cover various public benefits, including veterans’ benefits and unemployment compensation, with specific residency requirements for full protection.

Critical filing requirements for Michigan residents:

- Provide complete financial disclosure

- Complete pre-filing credit counseling

- Gather all necessary financial documentation

- Pay required filing fees (typically $338 for Chapter 7)

- Attend mandatory court hearings

Special considerations exist for homestead exemptions. Filers must typically own their home for 1,215 days to claim full state exemptions; otherwise, federal limits apply. Understanding these nuanced requirements is crucial for successfully navigating the bankruptcy process and protecting your financial future.

Financial Implications, Rights, and Risks

Bankruptcy represents a complex financial decision with profound long-term consequences. The immediate relief of an automatic stay provides critical protection from creditor actions, temporarily halting foreclosures, wage garnishments, and collection attempts. However, this legal shield comes with significant financial trade-offs that require careful consideration.

Key financial implications of bankruptcy include:

- Immediate cessation of creditor collection activities

- Potential discharge of unsecured debts

- Mandatory asset evaluation and potential liquidation

- Long-term credit report impact

- Restrictions on future lending opportunities

Different bankruptcy chapters carry distinct credit reporting timelines. Chapter 7 remains on credit reports for 10 years, while Chapter 13 stays for seven years after plan completion. This extended credit impact can significantly influence future financial opportunities, including loan approvals, interest rates, and housing applications.

Important financial risks to consider:

- Potential loss of non-exempt personal assets

- Reduced credit score

- Difficulty obtaining new credit

- Potential employment background check challenges

- Emotional and psychological stress

Additional questions about bankruptcy risks can help individuals make informed decisions. While bankruptcy offers a financial reset, it is not a consequence-free solution. Careful evaluation of personal financial circumstances, long-term goals, and alternative debt management strategies is crucial before proceeding with a bankruptcy filing.

Move Forward from Overwhelming Debt with Expert Michigan Bankruptcy Guidance

If you are struggling with unmanageable debt and feeling uncertain about whether Chapter 7, Chapter 13, or another path is right for you, you are not alone. Many Michigan residents feel the weight of creditor calls, fear for their homes, and worry about lasting impacts on their future. Understanding bankruptcy options and exemptions is an important first step, but choosing the right solution requires careful attention to your unique circumstances. The experienced attorneys at Frego & Associates are committed to helping you break free from financial hardship.

Take the first confident step by visiting our blog posts about bankruptcy for more clarity on the paths discussed in this article. If you are concerned about protecting your house, learn about available homestead exemptions in Michigan. Ready for clear answers and a supportive team on your side? Contact Frego & Associates now to schedule your free consultation or request a personalized bankruptcy evaluation. Take control of your financial future today at Frego Law.

Frequently Asked Questions

What is bankruptcy, and when should I consider filing for it?

Bankruptcy is a legal process that helps individuals and businesses eliminate or restructure their financial obligations when they can no longer make monthly payments. It should be considered after exhausting other financial strategies like budgeting and credit counseling.

What are the main differences between Chapter 7 and Chapter 13 bankruptcy?

Chapter 7 bankruptcy allows for rapid discharge of most unsecured debts through asset liquidation, while Chapter 13 bankruptcy involves creating a repayment plan to restructure debts over 3-5 years, allowing individuals to keep their assets.

How does the means test affect my eligibility for Chapter 7 bankruptcy?

The means test compares your household income to the state median income thresholds. If your income is below the median, you may qualify for Chapter 7. Those above the median may need to explore other options or undergo detailed calculations of disposable income to qualify.

What are the potential long-term effects of filing for bankruptcy?

Filing for bankruptcy can significantly impact your credit report, remaining on it for up to 10 years for Chapter 7 and 7 years for Chapter 13. It may also lead to difficulties in obtaining new credit, housing, or employment during the recovery period.