Job Loss in Michigan and Options for Bankruptcy

Losing your job in Michigan can turn a manageable life upside down in an instant. Suddenly, bills keep piling up while your income vanishes, setting off a stressful financial crisis that’s hard to control. Research shows job loss doesn’t just empty your wallet, it fuels riskier choices like gambling or payday loans, making things worse. This guide explains how bankruptcy offers a path to relief and a fresh start when debt feels impossible to escape.

Key Takeaways

| Point | Details |

|---|---|

| Job Loss Impacts Financial Stability | Losing a job not only eliminates income but also leads to immediate financial instability and poor decision-making under stress. |

| Bankruptcy as a Solution | Bankruptcy can be filed even without current income, offering a legal way to address overwhelming debts. |

| Understand Bankruptcy Options | Chapter 7 provides fast relief through debt discharge, while Chapter 13 offers a structured repayment plan, each suited to different financial situations. |

| Eligibility and Exemptions Matter | The means test determines bankruptcy eligibility, and understanding exemptions allows you to protect essential assets during the process. |

How Job Loss Triggers Financial Crisis

Job loss hits differently than most financial setbacks. When you lose your income, you don’t just lose money flowing in each month; you lose your financial stability almost instantly. What started as a steady paycheck becomes zero overnight, while your bills, mortgage payments, and daily expenses don’t pause or shrink to match your new reality.

This immediate gap between what you owe and what you have creates the first shock. But the real cascade begins when this disruption forces you to make decisions you normally wouldn’t make, decisions that compound the damage far beyond that initial lost income.

Research on job loss and risky financial behavior reveals something troubling: unemployment doesn’t just drain your bank account, it changes how you think about money. Stressed and desperate, people who’ve lost jobs show higher rates of risky financial decisions. They spend more on lotteries and gambling, hoping for a quick fix.

They make impulsive purchases. They delay paying bills to stretch remaining funds. These aren’t character flaws; they’re predictable responses to financial panic. A displaced worker facing mounting debt might take on payday loans with crushing interest rates, or max out credit cards on essentials, all while hoping to land a new job before the debt becomes unmanageable. The problem: that hope often doesn’t materialize as quickly as needed.

The domino effect happens fast. Without income, credit card balances grow. Medical bills pile up if you lose health insurance coverage. Late payments trigger penalties and higher interest rates. Your credit score drops, making it harder and more expensive to borrow money for legitimate needs. Creditors begin calling. Collection notices arrive. Family stress peaks.

Within months, many Michigan workers find themselves facing not just unemployment but also serious debt, damaged credit, and a sense that the situation has spiraled beyond their control. Displaced workers experience significant income declines and employment prospect challenges that trigger cascading financial crises across entire families. The longer the job search stretches, the worse these ripple effects become.

Here’s a summary of common financial risks triggered by job loss and ways bankruptcy can help mitigate them:

| Financial Risk After Job Loss | Typical Impact | How Bankruptcy Can Help |

|---|---|---|

| Unpaid bills accumulate | Late fees, growing debt | Discharge eligible debts, halt fees |

| Credit score drops | Harder, costly borrowing | Stops further damage, aids recovery |

| Creditor harassment | Frequent calls, lawsuits | Automatic stay stops contact |

| Asset loss threats | Foreclosure, repossession | Protects key assets via exemptions |

Pro tip: If you’ve recently lost your job, create an immediate budget prioritizing essential expenses like housing, food, and utilities, then contact a bankruptcy attorney before taking on high-interest debt or making risky financial decisions that could trap you further.

Bankruptcy Options After Losing Your Job

When job loss hits, bankruptcy might sound like admitting defeat, but it’s actually a legal tool designed to help people in exactly your situation. Here’s what matters: you can file for bankruptcy even if you’re currently unemployed or have zero income coming in. The law recognizes that job loss is a legitimate trigger for financial distress, and courts understand this reality. Many Michigan residents don’t realize this because they assume bankruptcy requires you to have income or a job lined up. That’s not how it works. What matters is your financial situation now, not what you hope to earn next month.

The tricky part involves the means test, which bankruptcy courts use to determine eligibility. This test compares your income over the previous six months, not just your current situation. If you earned $50,000 over the past six months but just lost your job last week, the court will still consider those earnings when evaluating your case.

This can complicate things if you’re trying to file Chapter 7 immediately after job loss while your recent income was still substantial. But here’s where it gets important: job loss qualifies as a special circumstance that courts recognize and adjust for. You can explain the sudden income drop to the judge, and they factor this into their decision. Filing bankruptcy while unemployed remains possible when you have legitimate reasons and meet the requirements, even if your path to eligibility isn’t straightforward.

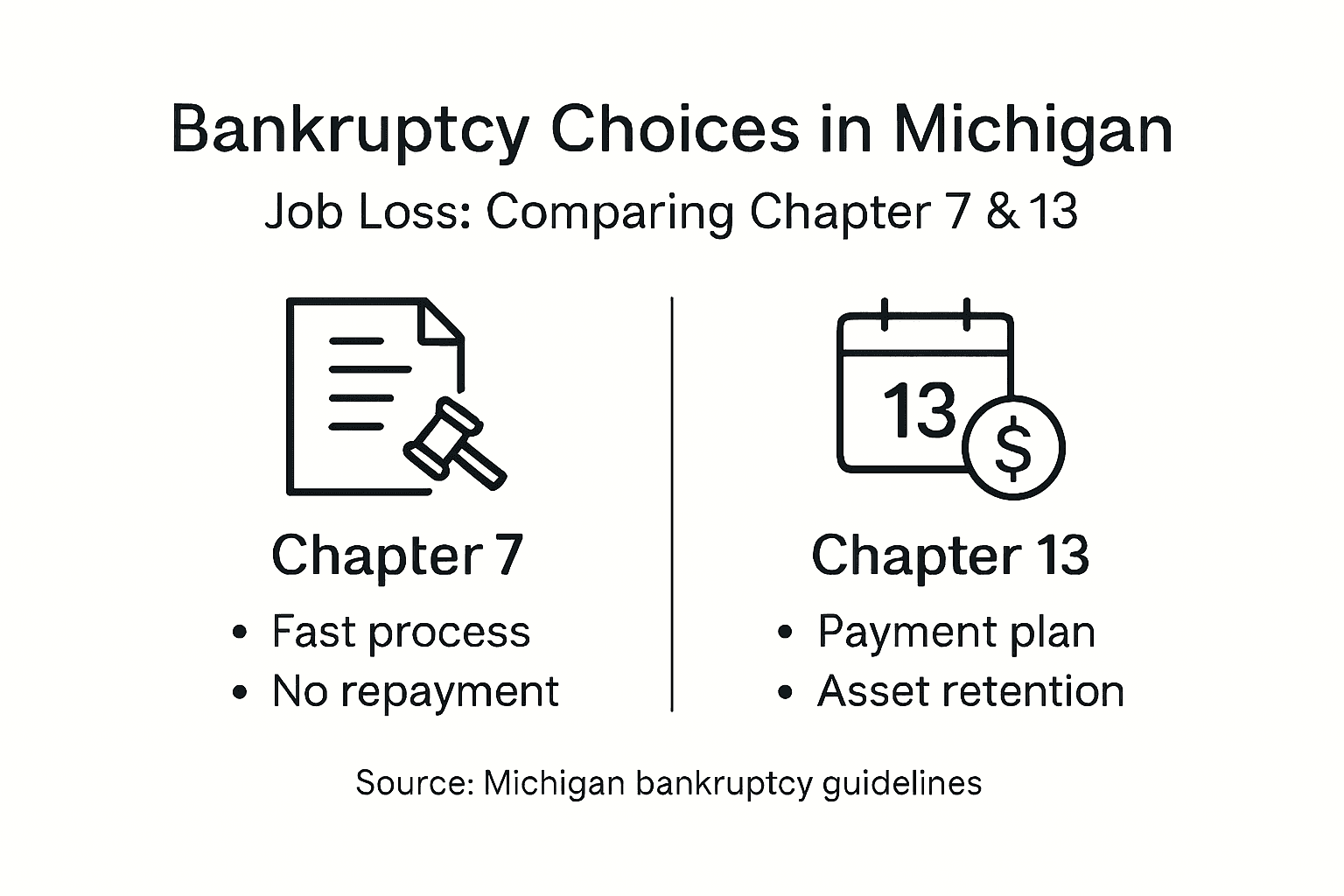

Your two main options are Chapter 7 and Chapter 13 bankruptcy. Chapter 7 liquidates eligible assets and eliminates most debts in about three to six months, which moves fast and gives you breathing room sooner. Chapter 13 restructures your debts into a manageable repayment plan over three to five years, which preserves your assets but requires you to have some income.

Without a job, Chapter 7 often makes more sense immediately, though Chapter 13 becomes viable once you secure new employment. Both options trigger an automatic stay, which stops creditors from calling, suing, or pursuing collections the moment you file. That protection alone can give you weeks or months to stabilize before dealing with creditors again. Understanding how filing bankruptcy affects employment helps you plan your next steps strategically.

Pro tip: File bankruptcy before maxing out credit cards or taking payday loans, since these newer debts might not discharge, and you’ll want the maximum fresh start when your case closes.

Chapter 7 and Chapter 13 Differences

Chapter 7 and Chapter 13 are two completely different paths through bankruptcy, and which one fits your situation depends on your income, assets, and how quickly you need relief. Think of Chapter 7 as the fast track: you liquidate nonexempt assets, discharge most unsecured debts, and walk away with a fresh start in three to six months.

Chapter 13 is the structured repayment plan: you keep your assets but commit to paying back a portion of your debts over three to five years through a court-approved plan. The choice between them shapes everything about your bankruptcy experience, from how long you’re in the system to what happens to your house, car, and other property.

Chapter 7 works best if you have little income and few assets to protect. The bankruptcy court runs you through a means test comparing your income to Michigan’s median household income. If you fall below the threshold, you qualify for Chapter 7, and the trustee sells off nonexempt property to pay creditors what they can.

Most of your unsecured debt (credit cards, medical bills, personal loans) gets discharged completely. However, Chapter 7 requires passing a means test based on income calculations, which is why job loss actually helps your eligibility. You lose the debt burden fast, but you might lose assets in the process. The tradeoff is speed and relief versus potentially surrendering property.

Chapter 13 is better if you have steady income, want to keep assets like your house or car, or need to catch up on missed payments. Instead of liquidation, you propose a repayment plan to the court.

You pay what you can afford each month for three to five years, and at the end, any remaining eligible debts get discharged. This works especially well for homeowners facing foreclosure or car owners with underwater loans. The catch: you need a reliable income to make those monthly payments, and you stay in bankruptcy longer. Chapter 13 debt reorganization protects property better than Chapter 7 because you’re restructuring debt rather than liquidating assets.

Quick Comparison

| Factor | Chapter 7 | Chapter 13 |

|---|---|---|

| Timeline | 3-6 months | 3-5 years |

| Best for | Low income, minimal assets | Stable income, assets to protect |

| Asset liquidation | Often required | None |

| Property protection | Limited | Strong |

| Debt discharge | Most unsecured debts | Remaining debts after plan |

| Income requirement | Below median | Above median |

After job loss, Chapter 7 typically makes more sense immediately since you have no income. Once you secure new employment, Chapter 13 becomes an option worth exploring if you want to protect assets you might otherwise lose.

Pro tip: If you own a home or car you want to keep, ask a bankruptcy attorney whether Chapter 13 makes sense once your employment stabilizes, since Chapter 7 might force you to sell these assets.

Eligibility Factors and Qualification Steps

Bankruptcy isn’t a free-for-all. The courts have specific eligibility requirements you need to meet, and understanding them upfront saves you from wasting time or money on a case that won’t qualify. The main gatekeeper is the means test, a federally mandated calculation that determines whether you can file Chapter 7 or get steered toward Chapter 13.

This test compares your average income over the past six months against Michigan’s median household income for your family size. If you’re below the median, you generally qualify for Chapter 7 presumptively, meaning you pass without additional scrutiny. If you’re above it, the court digs deeper into your expenses and disposable income to see if Chapter 13 makes more sense for you. Job loss actually works in your favor here because it typically drops your income below the threshold quickly.

Michigan bankruptcy filing requires mandatory credit counseling before you even submit paperwork to the court. You’ll attend an approved credit counseling course, usually online and taking about one to two hours, covering budgeting basics and debt management alternatives. This isn’t optional, and courts won’t accept your case without proof of completion.

After you file, you’ll attend a meeting of creditors (also called the 341 meeting), where a bankruptcy trustee asks you questions about your income, debts, and assets under oath. This sounds intimidating, but is usually straightforward, especially if you’re honest about your job loss and current situation. Then comes the mandatory debtor education course, another approved program focusing on financial management and rebuilding credit. Only after completing this can your debts actually be discharged.

What the Court Actually Checks

When evaluating your case, courts look at specific factors beyond just income. They examine your recent tax returns, bank statements, and employment history. They want to see that your financial crisis is genuine and not a strategic move. If you earned $70,000 six months ago but just lost your job, that’s a legitimate special circumstance courts understand.

They also check whether you have assets worth protecting, whether you’re current on child support or alimony, and whether you’ve filed bankruptcy before (which affects timing for discharge). Being transparent about everything strengthens your case rather than weakening it.

The Step-by-Step Process

- Complete credit counseling from an approved agency

- Gather financial documents (tax returns, pay stubs, bank statements, creditor statements)

- File your bankruptcy petition with the court

- Attend the meeting of creditors with the bankruptcy trustee

- Complete debtor education course

- Receive your discharge order

The entire process typically takes three to six months for Chapter 7 and three to five years for Chapter 13, depending on complexity and whether creditors challenge anything.

Pro tip: Start gathering your financial documents immediately after job loss, and enroll in credit counseling as soon as possible since you need proof of completion before filing, which gives you time to organize everything else.

Risks, Protections, and Common Pitfalls

Bankruptcy is a powerful tool, but like any powerful tool, it comes with real consequences you need to understand before pulling the trigger. The biggest risk everyone focuses on is credit damage. Your bankruptcy stays on your credit report for seven to ten years, and yes, it tanks your credit score significantly, sometimes by 130 to 200 points, depending on where you started.

This means higher interest rates on future loans, difficulty renting apartments, and potentially higher insurance premiums. But here’s what many people miss: your credit score starts recovering the moment your case closes, and responsible behavior rebuilds it faster than you might think. Some filers see their scores bounce back to acceptable ranges within two to three years because bankruptcy eliminates the debt burden that was dragging them down.

Bankruptcy provides protection from creditor actions like wage garnishment and lawsuits, which is one of its most valuable features after job loss. The automatic stay kicks in the moment you file, and creditors must stop calling, suing, and threatening collections immediately. This alone gives you breathing room to stabilize.

However, not all debts are discharged in bankruptcy. Student loans typically survive unless you prove undue hardship (a very high legal bar). Child support and alimony don’t disappear. Recent tax debts might stick around. Secured debts like mortgages and car loans don’t vanish either, though Chapter 13 can help you catch up on missed payments. Many filers assume everything goes away and feel blindsided when they learn otherwise.

Common Pitfalls That Derail Cases

One mistake people make constantly is filing too quickly without proper legal guidance. You might miss exemptions that could protect assets, or file under the wrong chapter because you didn’t understand your options. Another pitfall is running up new debt right before filing, thinking it will discharge. Courts scrutinize recent charges for cash advances, luxury purchases, and gambling.

These debts often don’t discharge if the trustee or creditors challenge them. A third pitfall involves hiding assets or income. This is fraud. Courts catch it, and you lose your discharge entirely. Being honest might mean losing some assets, but dishonesty means losing everything and potentially facing criminal charges.

What You Actually Keep

Bankruptcy law in Michigan allows you to exempt certain assets from liquidation. Your primary residence has homestead exemption protections. Your car up to a certain value, stays protected. Retirement accounts like 401(k)s and IRAs are largely untouchable. Essential household items, clothing, and tools of your trade have exemptions. Personal property under specific dollar limits gets protected. Understanding these exemptions before filing means you can structure your case to maximize what you keep.

Below is a reference table outlining Michigan’s bankruptcy exemptions and what you typically keep:

| Asset Type | Typical Exemption Protection | What You May Lose |

|---|---|---|

| Primary residence | Up to the homestead exemption | Value above exemption |

| Vehicle | Up to a set dollar amount | Luxury vehicles, excess value |

| Retirement accounts | Most protected by law | Loans against accounts |

| Personal property | Clothing, appliances, tools | High-value jewelry or collectibles |

Pro tip: Before filing, consult with a bankruptcy attorney about exemptions specific to your situation, since protecting the right assets now prevents surprises during your case.

Find Financial Relief After Job Loss with Expert Bankruptcy Help

Losing your job in Michigan creates urgent financial challenges that can feel overwhelming. Struggling with mounting debts, creditor calls, and fear of losing your assets like your home or car makes it hard to find a clear path forward. If you are facing these risks or are uncertain about Chapter 7 versus Chapter 13 bankruptcy options, you are not alone.

By understanding terms like the means test and homestead exemption, you can regain control and protect what matters most while eliminating burdensome debts.

Frego & Associates helps Michigan residents navigate these complex bankruptcy decisions with empathy and expertise. Learn how bankruptcy can provide an automatic stay from creditor harassment, discharge qualifying debts, and secure important exemptions. Protect your credit by accessing trusted resources by reading Credit, and understand how local property protections apply on our Homestead Exemption page.

Don’t wait until debts overwhelm you or risky financial decisions take hold. Take the first step toward relief today by requesting a free bankruptcy consultation by calling 1(800)646-0075. Your fresh start is possible with the right bankruptcy lawyer by your side.

Frequently Asked Questions

What are the main bankruptcy options available after losing a job?

You primarily have two options: Chapter 7 and Chapter 13 bankruptcy. Chapter 7 allows for the liquidation of certain assets to eliminate most debts quickly, while Chapter 13 involves a structured repayment plan to keep your assets and pay back a portion of your debts over three to five years.

Can I file for bankruptcy if I am currently unemployed?

Yes, you can file for bankruptcy even if you are unemployed or have no income. Courts recognize job loss as a valid trigger for financial distress, and the evaluation considers your financial situation at the time of filing.

How does job loss affect my eligibility for Chapter 7 bankruptcy?

Job loss can actually help your eligibility for Chapter 7 because it often reduces your income below the median threshold. You will need to pass the means test, which compares your income from the last six months against the median household income for your state.

What protections does bankruptcy provide after job loss?

Bankruptcy offers protections such as an automatic stay on creditor actions, stopping calls and collections immediately upon filing. It can allow you to discharge eligible debts, protect essential assets, and provide breathing room to stabilize your finances.